MileValue is part of an affiliate sales network and receives compensation for sending traffic to partner sites, such as CreditCards.com. This compensation may impact how and where links appear on this site. This site does not include all financial companies or all available financial offers. Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more.

Note: Some of the offers mentioned below may have changed or are no longer be available. You can view current offers here.

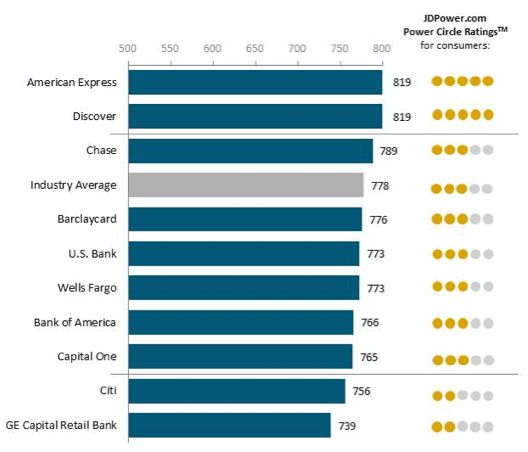

The J.D. Power 2014 U.S. Credit Card Satisfaction Study concludes that American Express and Discover have the highest customer satisfaction of any credit card issuers.

The study measures customer satisfaction with credit card issuers by examining six factors:

- interaction

- credit card terms

- billing and payment

- rewards

- benefits and services

- problem resolution

American Express has been #1 for all eight years of the study, and this year for the first time, it was tied for the top spot with Discover.

Interestingly, overall satisfaction with credit cards is at a record-high, surpassing last year’s record high. “Much of the bump is likely due to issuers piling on rewards, hoping to stand out from competitors, says Jim Miller, senior director of banking services at J.D. Power.”

The study has some very interesting nuggets for those of us who primarily use credit cards to earn miles and points.

- What are my favorite findings of the study?

- What is my ranking of issuing banks?

How American Express and Discover Got the Highest Scores

The top-ranked banks differ heavily in credit card strategy.

“American Express offers 21 cards aimed at different customer segments—some with annual fees and some without—and an array of reward options ranging from cash-back to travel rewards. Its customers tend to be more affluent, spend more and are less likely to carry a balance than customers of other card issuers.”

My Takeaway: Since AMEX makes less off of interest charges, it has to make more off of swipe fees. That’s why it has the highest swipe fees, and why the mom-and-pop stores around town won’t take AMEX cards.

“Discover’s strategy focuses on a single card with cash-back rewards and no annual fees. Discover serves a broad customer base and offers tools to help its customers manage their spending and debt, and provides its cardholders their credit score free of charge.”

My Takeaway: That would be the Discover it®. It offers 1% back on all purchases, 5% back on quarterly rotating categories, and 5-20% back through the ShopDiscover portal.

How Many Consumers Switch Cards and Why?

“Even with record-high customer satisfaction, 10 percent of customers have switched their primary card in 2014, up from 8 percent in 2013. Among those who switched cards, 42% did so for a better rewards program. ”

My Takeaway #1: Very few people switch cards. Inertia is why you see someone plugging away day after day for years with their Delta card, for instance, instead of opening one of the several cards that are better for earning Delta miles.

My Takeaway #2: The main reason people switch cards is because of a better rewards program. That’s the main reason I switch cards too.

My Takeaway #3: There’s not much that card companies can do to limit this switching. People will change even if the rewards programs don’t because no single rewards program is best for all of a person’s travel goals. For instance, the Starwood Preferred Guest program is the best for earning points than can be used for international first class. The Arrival miles program is best for earning miles that can be used for domestic economy. If your goal switches between the two, you’ll want to switch cards.

How to Improve Rewards Program Satisfaction without Improving Rewards

Obviously we’d all love a program more if the rewards got better, but education is another way to make people love a rewards program more–and it’s probably a lot cheaper for the issuing banks.

”Improved understanding of their current rewards programs may prevent customers from shopping for a new primary card. The percentage of customers who say they ‘completely’ understand how to earn rewards has increased to 63 percent in 2014 from 59 percent in 2013.”

I can only assume that the 4% of people who are new to the “completely understand” camp are MileValue readers. 😉

By the way if you don’t completely understand your rewards programs, sign up to receive one free daily email every morning with all of MileValue’s posts that day. And forward an email to your friends for them to sign up.

What People Don’t Know about Their Rewards

“However, in 2014, 21 percent of customers don’t know if they can earn extra rewards for specific purchases; 43 percent don’t know if their rewards have an annual maximum limit; and 30 percent don’t know if their rewards have an expiration date.”

Let me answer those questions:

- If you don’t know a card’s category bonuses, google that card. The category bonuses are key to maximizing rewards, which is why I always cover them when I discuss a new card offering.

- I can’t think of any cards that limit the points/miles you can earn at the base 1x rate. Why would there be a limit? The issuing bank is making money off you if all your spending is at the base rate. Some cards cap the points you can earn from category bonuses. For instance Chase caps the 5x categories on the Inks and Freedom.

- The Complete Guide to Miles and Points Expiration

Full Ratings from J.D. Power

On a 1,000 point scale:

My Ratings

My Ratings

My ratings are based only on the quantity and quality of rewards cards offered to US consumers, not at all on the other five categories considered by J.D. Power.

- Chase: I can think of at least ten cards worth getting, most with 50,000 point sign up bonuses. The Ultimate Rewards program is top tier; the airline cards have big sign up bonuses; Chase has great personal and business cards; and there are even great hotel cards.

- American Express: Between the Delta, SPG, Platinum, Gold, and EveryDay cards–most of which have personal and business versions–there are a lot of rich offers.

- Citi: The American Airlines cards and Hilton cards are nice, and I’m really glad that the ThankYou cards now earn points transferable to nine airlines.

- Barclaycard: US Airways cards and Arrival cards are the biggest, but I also love the niche cards: the Lufthansa card, Hawaiian cards, and Frontier card.

- US Bank: Club Carlson cards and FlexPerks cards

How would you rate the top five issuing banks?

Just getting started in the world of points and miles? The Chase Sapphire Preferred is the best card for you to start with.

With a bonus of 60,000 points after $4,000 spend in the first 3 months, 5x points on travel booked through the Chase Travel Portal and 3x points on restaurants, streaming services, and online groceries (excluding Target, Walmart, and wholesale clubs), this card truly cannot be beat for getting started!

Editorial Disclaimer: The editorial content is not provided or commissioned by the credit card issuers. Opinions expressed here are the author’s alone, not those of the credit card issuers, and have not been reviewed, approved or otherwise endorsed by the credit card issuers.

The comments section below is not provided or commissioned by the bank advertiser. Responses have not been reviewed, approved, or otherwise endorsed by the bank advertiser. It is not the bank advertiser’s responsibility to ensure all questions are answered.

There is no way 63% of people ‘completely’ understand how to earn rewards through credit cards. I wouldn’t even say that I understand it completely, yet everyone I know in my day-to-day life thinks I’m some sort of prodigy on the subject. Most people put all their spending on one no-fee card that earns 1% cash back, and feel great about the $150 in free gift cards they got last year. Makes me cringe sometimes… 🙂

I read that as “completely understand” earning and redeeming on their card’s rewards program. I also think many people who think they get it don’t, but if you just have one fixed-value, bank-point card, it should be pretty easy to understand your program.

Amex is number one for me – by a country mile. Chase has sign up bonuses but Amex has category bonuses that overwhelm signup bonuses if you do any meaningful volume. And thanks to Citi churnabilty, it’s #2. Then Chase, with a tie for Barclays and USBank of #3. WF is at the bottom despite their 5x card. The rest of the issuers are worthless.

The interesting extra question would have been… how many people changed their principal card MORE THAN ONCE during the year !!!

I’d love to know. I have..

Barclaycard is horrible. I was able to call cap one about usubg travel eraser for a few transactions that didn’t post as travel on the venture. Never can do that with Barclay. The stink!

I’ve heard people have success with Barclaycard doing that for them.